Educational Article

⚠️ Important Disclaimer

Mutual fund investments are subject to market risks, including the possible loss of principal. This article is purely educational and does not constitute investment advice, recommendation, or solicitation. Past performance is not indicative of future results. Actual returns may be higher, lower, or negative. Do not make any investment decisions based solely on this content. This content is part of distribution-related education and does not constitute SEBI-registered investment advice. Always read the Scheme Information Document (SID) and Key Information Memorandum (KIM) carefully before investing. For personalised guidance, consult an AMFI-registered Mutual Fund Distributor or SEBI-registered Investment Advisor.

About the Author

Amit Verma | AMFI Registered Mutual Fund Distributor (ARN-349400)

Verifiable at amfiindia.com

I am an AMFI-registered Mutual Fund Distributor helping Indian investors build simple, goal-based portfolios through Regular Plans. This guidance is provided via Regular Plans offered through AMFI-registered distributors; no comparison with other plan types is made in this article.

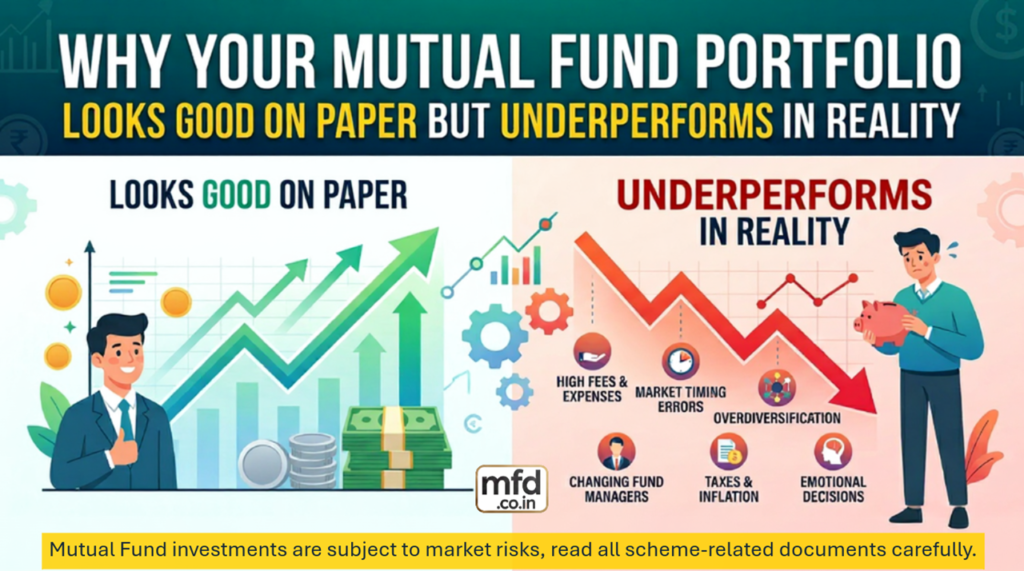

Quick Summary – Read This First

| Issue | How It Looks on Paper | What Is Actually Happening |

|---|---|---|

| Overlapping holdings | “I own 12 diversified equity funds” | Most funds hold the same top 10–15 large cap companies |

| Cumulative cost drag | “Each fund has a reasonable expense ratio” | Multiple fees across many funds compound into a significant long-term drag |

| No goal alignment | “I am invested for the long term” | No fund is clearly linked to a specific goal and timeline |

| Behavioural interference | “I review and rebalance when needed” | Constant noise from too many funds drives emotional, reactive decisions |

| Performance dilution | “I have many well-performing funds” | Strong performers are averaged down by mediocre or overlapping ones |

| Review fatigue | “I monitor my portfolio regularly” | 20+ funds are too many to review meaningfully – reviews become superficial or stop altogether |

- This is educational guidance only; individual suitability always depends on your personal financial situation and goals. All investments remain subject to market risk.

There is a particular kind of investor frustration that I encounter regularly in practice. It sounds something like this:

“I have been investing consistently for six years. I have 18 funds across different categories, different fund houses, a mix of equity and hybrid. On the app, it looks well-organised and diversified. But when I actually calculate what I have earned versus what I put in – and compare it to what a simpler approach might have delivered – the numbers are disappointing. What is going wrong?”

What this investor is experiencing has a name. The financial industry calls it diworsification – a portfolio that looks sophisticated and diversified on the surface, but is actually working against the investor through overlapping holdings, unnecessary costs, behavioural noise, and the absence of any clear purpose for most of what it contains.

This is not a rare problem. It is one of the most common patterns in Indian mutual fund investing in 2026. It affects investors who are genuinely engaged, genuinely trying to do the right thing, and genuinely confused about why the outcomes are not better. The problem is almost never bad funds or bad luck. It is almost always a structural problem, a portfolio built through accumulation rather than architecture.

This article explains the specific mechanisms through which good-looking portfolios underperform. It draws on the regulatory context of 2026, including SEBI’s recent actions specifically addressing portfolio overlap. And it gives you a practical, actionable framework for how to identify whether your portfolio has this problem and what to do about it.

This is educational guidance only. Individual suitability depends on your personal financial situation, goals, and risk profile.

A Tale of Two Portfolios – The Same Money, Very Different Outcomes

Before getting into the mechanics, let me illustrate the contrast that motivates this article. The following comparison is simplified and illustrative. Actual outcomes will vary significantly based on market conditions, fund selection, and investor behaviour.

Portfolio A: The accumulated collection (18 funds)

This portfolio was built over eight years through a combination of app recommendations, friend suggestions, NFO subscriptions, and thematic fund additions. Each addition seemed reasonable at the time. The portfolio now spans large cap, flexi cap, mid cap, small cap, multiple thematic and sectoral funds, a couple of hybrid funds, and one debt fund. Different fund houses are represented. The category spread looks impressive.

What the investor experiences: Constant noise, some funds up, some down, some flat, some requiring attention. Annual reviews are overwhelming and usually incomplete. During market corrections, multiple funds show significant declines simultaneously, creating disproportionate anxiety. The overall portfolio return, when calculated, is unremarkable relative to what a simpler structure might have delivered.

Portfolio B: The goal-based structure (7 funds)

This portfolio was built around three specific goals with three different timelines. It has a liquid fund for the emergency bucket, a multi-asset fund for the medium-term balance bucket, and a combination of flexi-cap, index, and mid-cap funds for the long-term growth bucket. Each fund has a named purpose. The manager knows exactly which goal each SIP is serving.

What the investor experiences: Clarity. Annual review takes twenty-five minutes. During market corrections, each fund’s decline is contextualised by its goal timeline, the growth bucket is down, but the goal is 22 years away. The cumulative expense ratio is meaningfully lower. The portfolio’s actual returns are not dramatically different from Portfolio A in any given year, but the consistency of staying invested and not making reactive decisions compounds materially over time.

The difference between these two portfolios is not the individual funds chosen. It is the architecture, the presence or absence of a clear purpose for every rupee invested.

Reason 1: Pseudo-Diversification – The Overlap Trap

The most structurally important reason a cluttered portfolio underperforms is that it is far less diversified than it appears.

India’s equity market has a naturally concentrated large-cap universe. The top 15–20 companies by market capitalisation dominate most equity fund benchmarks because these are the most liquid, most widely held, and most heavily weighted businesses in the country. Every equity fund that has meaningful large cap exposure, and most equity funds do, because large cap stocks provide stability and liquidity, will hold a significant proportion of these same companies.

When you own five or six equity funds across large cap, flexi cap, and multi cap categories, you are almost certainly owning the same top five or six companies multiple times. Your apparent diversification across fund houses and fund managers often translates, at the underlying stock level, to ownership of the same narrow set of companies repeatedly, simply under different scheme names.

The industry uses the term diworsification specifically to describe this situation: a portfolio that appears diversified by the number of schemes it contains but is actually concentrated in its underlying holdings. Industry research platforms that track portfolio overlap consistently identify 60–70% overlap between two equity funds in the same category as “very high,” noting that at this level you are not adding meaningful diversification by holding both, you are adding cost and complexity while duplicating exposure.

SEBI acknowledged the scale of this problem explicitly in its February 2026 mutual fund categorisation circular. The regulator specifically addressed thematic and sectoral funds, which proliferated enormously during the NFO boom of 2021–2024, by introducing mandatory overlap limits. Under these new rules, thematic and sectoral funds from the same fund house cannot have more than 50% portfolio overlap with other equity schemes from the same house. Overlap must be calculated quarterly using daily portfolio values and disclosed monthly on fund-house websites. The regulatory intervention confirms that portfolio overlap had grown to a structural problem requiring formal correction.

What this means for your portfolio: Adding the sixth equity fund does not add the sixth layer of genuine diversification. It adds the sixth layer of ownership of the same five large cap companies, while adding management fees, another monthly factsheet to track, and one more data point generating noise during market movements. You are paying more to get less uniqueness.

How to check your own overlap: The monthly factsheet of every mutual fund lists its top 10 holdings. For any two equity funds in your portfolio, comparing their top 10 holdings side by side takes approximately five minutes. If you see the same four or five companies in both funds’ top holdings lists, you have meaningful overlap. If you see this pattern across three, four, or five funds, your portfolio is significantly less diversified than the number of schemes suggests.

Reason 2: Cumulative Cost Drag That Compounds Against You

Every mutual fund scheme charges its own expense ratio, the annual fee deducted from the fund’s assets that covers management, administration, and distribution costs. When you hold many funds, each with its own expense ratio, the weighted average cost of your total portfolio tends to be higher than it needs to be.

The problem compounds in two specific ways. First, accumulated portfolios tend to include more expensive fund types, thematic and sectoral funds carry higher expense ratios than broad equity funds, and fund of funds carry layered fees where you pay both the Indian fund’s charges and the underlying fund’s charges. Second, the mathematics of slightly higher annual costs over 15–30 years creates a gap in final corpus that is invisible in any single month but substantial over the full investment horizon.

The following table illustrates the long-term cost difference at a starting corpus of ₹10 lakh with an assumed 8% pre-cost annual return. These are illustrative calculations only, actual returns will vary.

| Annual Cost Difference | Effect After 15 Years | Effect After 20 Years | Effect After 30 Years |

|---|---|---|---|

| Extra 0.3% per year | ₹1.4 lakh reduction | ₹2.6 lakh reduction | ₹7.8 lakh reduction |

| Extra 0.5% per year | ₹2.3 lakh reduction | ₹4.4 lakh reduction | ₹13 lakh reduction |

| Extra 0.8% per year | ₹3.7 lakh reduction | ₹7.0 lakh reduction | ₹20+ lakh reduction |

Strictly illustrative – based on hypothetical 8% pre-cost return on ₹10 lakh. Actual returns may be significantly different. This is for demonstration of compounding impact only.

The extra cost of a cluttered portfolio, accumulated through thematic funds with higher expense ratios, redundant funds in the same category, and fund of funds with layered fees, is typically in the range of 0.4–0.8% per year relative to a clean, simplified portfolio. Over 20–30 years, that difference compounds into a material reduction in the wealth you actually accumulate. It does not show up as a loss on any monthly statement. It shows up as a smaller final corpus than the same investments at lower cost would have produced.

Reason 3: No Goal Alignment – The Structural Vacuum

This is perhaps the most consequential hidden problem, because it determines not just whether your funds perform well but whether you stay invested in them through the conditions required for them to compound.

When funds are added without a clear connection to a specific goal and timeline, “this one performed well recently,” “my colleague recommended it,” “the NFO seemed interesting”, there is no framework for what to do when anything changes. When markets correct, there is no contextual answer to the question “should I stop my SIP?” When a fund underperforms for a year, there is no basis for distinguishing between “this is temporary and I should hold” and “this fund has genuinely failed its purpose.” When a life event occurs, there is no clear way to understand which funds are affected.

Goal alignment creates the context that makes every market movement interpretable. Consider the same market correction from two perspectives:

Without goal alignment: “My portfolio is down 15%. I have 18 funds all showing declines. Everything feels wrong. I should stop SIPs until things stabilise.”

With goal alignment: “My growth bucket is down 15%, but my retirement goal is 23 years away, so these are cheaper units my SIP is buying. My balance bucket is in a multi-asset fund and is down only 5%. My emergency fund is in a liquid fund and is completely untouched.”

The second investor has no reason to change their behaviour. The first investor is likely to make at least one decision they will regret.

Goal alignment is also what makes the number of funds you own self-limiting in a healthy way. You genuinely cannot have 30 goals. If every fund requires a named goal and timeline to justify its presence, the portfolio naturally settles at a manageable size.

Reason 4: Behavioural Amplification – More Funds, More Noise, Worse Decisions

A portfolio of 20 funds generates 20 simultaneous signals. On any given day, and especially during market volatility, some are rising, some falling, some flat, some significantly below their category peers. This constant multi-directional noise creates a sustained decision-making pressure that a small, purposeful portfolio does not.

With many funds, there is always something validating whichever emotional impulse you are experiencing. If you are anxious about the market, there is always a fund showing a significant decline to confirm your worry. If you are feeling regret about missed opportunities, there is always a fund that has recently surged that you do not own. This noise makes disciplined behaviour harder to maintain, not because the investor lacks conviction, but because the portfolio structure is generating too many competing signals.

Specific behavioural traps that a cluttered portfolio amplifies:

Loss aversion becomes more intense because more funds showing simultaneous declines creates a feeling of pervasive loss, even when the total portfolio decline is manageable. The investor stops SIPs or redeems at exactly the moment they should be continuing.

Recency bias is amplified because with many funds, there are always recent strong performers visible in the portfolio that make current laggards look comparatively worse than they are in a long-term context.

Confirmation bias works perversely, with 20 funds, you can always find two or three that are doing well and use those as evidence that the portfolio is fine, while ignoring the majority that are underperforming.

Overconfidence can masquerade as sophistication, having many funds creates the impression of active, engaged management, even when no meaningful strategic decisions are actually being made.

A smaller, goal-mapped portfolio removes most of this noise. There are fewer signals, each one contextualised by a clear purpose, and the default response to volatility becomes “stay the course” rather than “do something.”

Reason 5: Performance Dilution – Winners Averaged Down by Mediocrity

In a portfolio of 15–20 funds, some are genuinely excellent performers over the long term. But if those excellent performers represent only a small fraction of the total portfolio, perhaps 10–15% combined, while the remaining 85% is spread across mediocre, overlapping, or purpose-less schemes, the excellent funds cannot meaningfully drive the portfolio’s overall return.

The mathematics is straightforward: if your two best funds together represent 15% of your portfolio and deliver 20% returns, while your remaining 18 funds average 10%, your total portfolio return is approximately 11.3%. If those same two best funds represented 40% of your portfolio, the total would be approximately 14%. The funds themselves have not changed, only how much of your portfolio they represent.

A focused portfolio of 5–8 well-chosen funds, each with clear purpose and appropriate allocation, allows your strongest investments to actually drive your outcomes rather than being diluted by schemes accumulated without strategic rationale.

Reason 6: Review Fatigue – The Complexity That Prevents Meaningful Oversight

Every investment portfolio requires periodic review, checking whether each fund remains appropriate for its goal, whether goal buckets are on track, and whether any rebalancing is warranted. The time required for a meaningful review scales with the number of funds.

A thorough annual review of 5–7 funds takes 20–30 minutes and covers everything that matters. A thorough annual review of 20+ funds takes well over an hour, requires comparing multiple factsheets, identifying numerous performance stories across different categories and market cycles, and making allocation judgments across holdings that are often difficult to differentiate. The result, predictably, is that most investors with cluttered portfolios either review infrequently, review superficially, or stop reviewing altogether.

When meaningful reviews stop, important signals go undetected: a fund that has consistently underperformed its category for three years, a goal bucket that has drifted significantly from its target allocation, a goal that is approaching its timeline without the de-risking that should have started two years earlier. These undetected problems quietly compound into meaningful underperformance and planning failures.

SEBI’s 2026 Action – Why Even the Regulator Is Addressing This

The scale of the portfolio overlap problem became significant enough that SEBI addressed it structurally in its February 2026 mutual fund categorisation circular. The regulator observed that the NFO boom of 2021–2024 had resulted in a proliferation of thematic and sectoral fund schemes, many with substantially overlapping portfolios, effectively the same core holdings packaged under different thematic labels and marketed as distinct products.

SEBI’s February 2026 circular introduced mandatory portfolio overlap limits specifically for thematic and sectoral equity funds. These funds cannot have more than 50% portfolio overlap with other equity schemes from the same fund house. Overlap is calculated quarterly using daily portfolio values and disclosed monthly on fund house websites. Existing schemes have a phased three-year compliance timeline.

This regulatory action matters directly for investors with cluttered portfolios. It confirms that the overlap problem is structurally real and significant. It also creates a natural review opportunity: investors holding multiple thematic or sectoral funds, particularly from the same fund house, may find that those funds are actively being required to differentiate their portfolios, making this a timely moment to assess whether all those funds genuinely serve distinct purposes in your own portfolio.

How Many Funds Does Your Portfolio Actually Need?

These are general educational guidelines only. Individual circumstances vary and consultation with a registered distributor is recommended.

By Portfolio Size

| Total Corpus | Typically Sufficient | Generally Maximum |

|---|---|---|

| Under ₹5 lakh | 3–4 funds | 5 funds |

| ₹5 lakh – ₹20 lakh | 4–6 funds | 8 funds |

| ₹20 lakh – ₹50 lakh | 5–8 funds | 10 funds |

| ₹50 lakh – ₹2 crore | 7–10 funds | 12 funds |

| Over ₹2 crore | 8–14 funds | 15 funds (with clear rationale) |

By Life Stage

| Life Stage | Typically Suitable Range | Primary Logic |

|---|---|---|

| Absolute beginner | 2–3 funds | Build habit and discipline; complexity is the enemy |

| Early career (25–35) | 4–6 funds | Emergency bucket + retirement SIP + one goal bucket |

| Mid career (35–50) | 6–9 funds | Multiple goals across different horizons |

| Pre-retirement (50–60) | 5–8 funds | Simplify; de-risking underway; fewer decisions better |

| Retirement (60+) | 4–6 funds | SWP structure; minimal complexity; income stability |

The Diminishing Returns Curve

| Number of Funds | Diversification Added | Cost and Complexity Added | Net Outcome |

|---|---|---|---|

| 1–3 | High | Low | High net value |

| 4–7 | Good | Moderate | Good net value |

| 8–12 | Marginal | Moderate-high | Borderline |

| 13–16 | Very little | High | Negative net value |

| 17+ | Essentially none | Very high | Clear drag on outcomes |

The Goal-Based Solution – How It Actually Works

The practical solution to diworsification is not removing funds randomly. It is rebuilding the portfolio around goals, so that every fund has a named purpose, a named timeline, and a role it is specifically designed to serve.

The Three-Bucket Framework

| Bucket | Time Horizon | Typically Suitable Fund Types | Recommended Fund Count |

|---|---|---|---|

| Safety | 0–3 years | Liquid, overnight, ultra-short duration | 1–2 |

| Balance | 3–8 years | Multi-asset, conservative hybrid, balanced advantage | 1–3 |

| Growth | 8+ years | Flexi-cap, index funds, large & mid cap, selective mid cap | 2–4 |

Total: typically 4–9 funds covering most investors’ complete goal landscape.

A Practical Illustration (Simplified, Illustrative Only)

| Goal | Horizon | Bucket | Fund Type |

|---|---|---|---|

| Emergency fund | Always available | Safety | Liquid fund |

| Child’s higher education | 12 years | Growth | Flexi-cap fund |

| Retirement | 24 years | Growth | Index fund + mid cap fund |

| Home down payment | 5 years | Balance | Multi-asset fund |

Five funds. Four goals. Every rupee has a job and a deadline.

When markets fall, the investor’s mental response shifts from “my portfolio is down” to something more precise and more manageable: “my retirement corpus is down, but I have 24 years and I am buying cheaper units today; my home down payment fund is in a multi-asset fund and is largely stable; my emergency fund is untouched.” That contextual clarity is the most powerful behavioural protection available.

A Practical Simplification Framework

These are general educational steps only. Portfolio changes involve individual circumstances and potential tax events. Always consult a registered distributor or SEBI-registered Investment Advisor before acting.

Step 1: Conduct an Honest Audit

List every fund you hold with: its category, current value, how long you have held it, and, the critical question, what specific goal it is serving. Where you cannot clearly answer the goal question, that is your first signal.

Step 2: Check for Overlap

For every equity fund pair in your portfolio, compare the top 10 holdings from each fund’s most recent monthly factsheet. Where you find the same three, four, or five companies in both funds’ top holdings, you have meaningful overlap. Where this pattern repeats across multiple pairs, you have structural redundancy.

Step 3: Evaluate Each Fund Against Clear Criteria

| Keep if | Consider exiting if |

|---|---|

| Consistent performance vs category peers over 5+ years | Persistent underperformance for 3+ consecutive years |

| Clear purpose linked to a specific goal and timeline | No clear purpose articulable |

| Expense ratio reasonable for its category | Elevated expense ratio, especially thematic or sectoral funds |

| Fund management stable | Frequent manager changes |

| Low or manageable overlap with other kept funds | High overlap with another fund you are retaining |

Step 4: Design a Tax-Efficient Consolidation Sequence

| Action | Timing Consideration |

|---|---|

| Stop SIPs into funds you intend to exit | No tax impact – can be done immediately |

| Identify holdings already past 12 months | These qualify for LTCG treatment at 12.5% above ₹1.25 lakh |

| Plan exits for holdings not yet 12 months old | Consider waiting for the 12-month threshold where meaningful gains exist |

| Use the ₹1.25 lakh annual LTCG exemption | Stagger exits across financial years to use the exemption each year |

| Consider booking losses where available | Realised losses in underperforming funds offset taxable gains elsewhere |

Tax rules are subject to change. Always consult a qualified tax professional before making redemption decisions.

Step 5: Redirect to the Simplified Structure

Once you have identified what you are keeping, redirect all SIPs and reinvested proceeds to your clean, goal-mapped portfolio. Review annually – the whole exercise should take 20–30 minutes once the structure is in place.

Illustrative Before and After

Strictly illustrative – does not represent any actual investor’s portfolio. Actual outcomes will vary.

Before: 20-Fund Accumulated Portfolio

| Category | Fund Count | Primary Problem |

|---|---|---|

| Large cap funds | 4 | Heavy overlap – same top 10 stocks across all four |

| Flexi cap funds | 3 | Very similar underlying portfolios |

| Mid cap funds | 2 | Moderate overlap |

| Small cap funds | 2 | Doubled up without rationale |

| Thematic/sectoral | 5 | High cost, high overlap between themes, no goal attached |

| Hybrid | 2 | Acceptable but unplanned |

| Debt | 2 | Acceptable |

Result: High overlap, elevated average expense ratio, 1.5+ hours to review properly, no goal mapping for most funds, disproportionate anxiety during corrections.

After: 7-Fund Goal-Based Portfolio

| Bucket | Fund Type | Purpose |

|---|---|---|

| Safety | Liquid fund | Emergency fund |

| Balance | Multi-asset fund | Medium-term goals |

| Growth | Flexi-cap fund | Retirement and long-term goals |

| Growth | Index fund | Core large cap exposure |

| Growth | Mid cap fund | Higher growth component |

| Debt | Short-duration fund | Stability allocation |

| Optional | Gold or multi-asset | Inflation hedge and diversification |

Result: Clear purpose for every fund, reduced average expense ratio, 20-minute annual review, genuine goal alignment, calmer market response.

Illustrative Metrics Comparison

| Metric | 20-Fund Portfolio | 7-Fund Portfolio |

|---|---|---|

| Average expense ratio | ~1.4% | ~0.9% |

| Illustrative annual cost saving (on ₹50L) | – | ~₹25,000 per year |

| Top holdings overlap | 70%+ | Below 30% |

| Annual review time | 1.5+ hours | 20 minutes |

| Goal clarity | None for most funds | Each fund has a named purpose |

Illustrative only. Actual expense ratios, costs, and outcomes will vary.

Common Rationalisations – And Why They Don’t Hold

“I am diversified across different fund houses.”

Fund houses are not the relevant unit of diversification, underlying stock holdings are. If multiple fund houses’ equity funds all hold the same top five companies in their portfolios, holding one from each house provides no additional diversification.

“Each fund has a different strategy.”

Strategies that appear distinct in marketing materials often converge significantly in practice. Always check actual holdings rather than strategy descriptions.

“I don’t want to pay capital gains tax to consolidate.”

Paying LTCG tax once to exit a fund that has been dragging your portfolio for three years is almost always more economically rational than holding it for several more years hoping for recovery. The opportunity cost of remaining in an underperformer typically exceeds the one-time consolidation tax. Staggering exits over two or three financial years using the annual LTCG exemption can reduce the tax burden significantly.

“I will review and decide later.”

Portfolio reviews that are perpetually deferred are reviews that never happen. Stop SIPs into funds you are uncertain about immediately, there is no tax impact from stopping a SIP, and conduct the review when you can. The separation of these two steps removes the urgency barrier.

“This fund will recover.”

Possibly. But the relevant question is whether the fund you are holding is the best use of that capital for your specific goal and timeline, or whether an alternative would serve the same goal more effectively. Opportunity cost, not hope, is the correct lens for evaluating an underperformer.

How a Registered Distributor Helps With This

As an AMFI-registered distributor, conducting portfolio audits and building simplified, goal-based structures is one of the most valuable services I provide for clients. These are educational and guidance-only services; all investments remain subject to market risk.

Specifically, a structured portfolio review involves: auditing every fund for goal alignment and overlap, calculating the estimated cost differential between the current structure and a simplified alternative, designing a tax-efficient consolidation sequence that uses the annual LTCG exemption strategically, and setting up the simplified goal-based portfolio with appropriate SIPs and step-up features.

The ongoing value is behavioural as much as structural: a simpler portfolio generates less noise, fewer emotional triggers, and a clearer framework for interpreting market movements. The investor who can say “my retirement bucket is down, but I have 20 years” responds very differently to a correction than the investor looking at a list of 22 declining funds with no clear context for any of them.

The Final Point

A portfolio that looks good on paper but underperforms in reality is almost never the result of bad funds or bad luck. It is the result of structure – a collection of schemes built through accumulation rather than architecture, without clear purpose for each holding, without a framework for maintaining discipline through market cycles, and with a cost and complexity profile that quietly works against compounding over years and decades.

The good news is that the fix is genuinely straightforward. It requires honesty about what each fund is actually doing for your goals, a willingness to simplify even when simplification requires a one-time tax event, and the discipline to maintain a smaller, cleaner structure through annual reviews rather than reactive daily monitoring.

The question to ask for every fund in your portfolio is simple: What specific goal is this serving, and when will I need that money? Where you cannot answer clearly, that is where the simplification work begins.

If you would like help conducting a structured portfolio audit, identifying overlaps, calculating hidden cost drag, and building a cleaner goal-based structure, I am here to help you work through it. Free 15-minute chat, no obligation, no pressure. This is purely distribution-related guidance; mutual fund investments are always subject to market risk. Do not make any investment decisions based solely on this conversation or this article – always read all scheme-related documents and consult appropriate professionals before acting.

About the Author

Amit Verma | AMFI Registered Mutual Fund Distributor (ARN-349400)

Verifiable at amfiindia.com

Ready to Fix Your Portfolio?

📱 WhatsApp: +91-76510-32666 – Free 15-min chat, no obligation

🌐 mfd.co.in/signup

✉️ planwithmfd@gmail.com

I am an AMFI-registered Mutual Fund Distributor helping investors build simple, goal-based portfolios through Regular Plans – including identifying and correcting portfolio clutter before it compounds into a meaningful long-term drag on wealth creation. This guidance is provided via Regular Plans offered through AMFI-registered distributors; no comparison with other plan types is made in this article.

Final Disclaimer

Mutual fund investments are subject to market risks, including risk of capital loss. This article is purely educational and does not constitute investment advice, recommendation, or solicitation. Past performance is not indicative of future results. Actual returns may be higher, lower, or negative. This content is part of distribution-related education and does not constitute SEBI-registered investment advice. Always read the Scheme Information Document (SID) and Key Information Memorandum (KIM) carefully before investing. For personalised guidance based on your financial situation, goals, and risk profile, consult an AMFI-registered Mutual Fund Distributor or SEBI-registered Investment Advisor. Do not make any investment decisions based solely on this article.

Before investing or making any portfolio changes, please read all scheme-related documents including the Scheme Information Document (SID) and Key Information Memorandum (KIM). This is purely distribution-related guidance; do not make any investment decisions based solely on this article or this conversation.